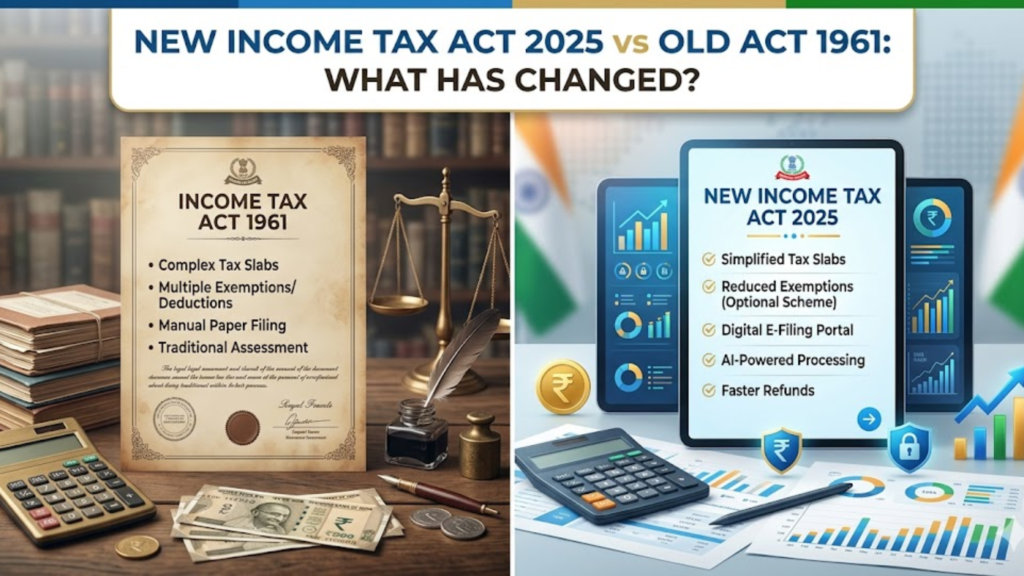

India’s taxation system is entering a new era with the introduction of the Income Tax Act, 2025, which replaces the decades-old Income Tax Act, 1961. Effective from 1 April 2026, this reform is not just a routine update—it represents a complete overhaul aimed at simplifying compliance, improving clarity, and reducing litigation.

For taxpayers, professionals, and businesses, understanding the differences between the old and new tax laws is essential for effective financial planning. This article provides a detailed comparison of the Income Tax Act 2025 vs Income Tax Act 1961, highlighting key changes, improvements, and their practical impact.

Need ITR Filing Help: Income Tax Return Filing Service

Why Was a New Income Tax Act Introduced?

The Income Tax Act, 1961 served India for over six decades. However, over time, it became increasingly complex due to:

- Frequent amendments

- Multiple interpretations by courts

- Outdated provisions

- Complicated legal language

To address these challenges, the government introduced the Income Tax Act, 2025 with the following objectives:

- Simplify tax laws and structure

- Use clear and easy-to-understand language

- Remove redundant and obsolete provisions

- Reduce legal disputes

- Improve ease of compliance

1. Simplified Structure and Language

Old Act (1961):

The earlier law was known for its complex structure, lengthy sections, and heavy use of legal jargon. Many provisions were difficult for the average taxpayer to understand without professional assistance.

New Act (2025):

The new Act adopts a simplified and structured approach, making it easier to read and interpret. Key improvements include:

- Shorter and clearer sections

- Logical grouping of provisions

- Reduced cross-referencing

- Easy-to-understand terminology

Impact:

Taxpayers will find it easier to understand their obligations, reducing dependency on experts for basic compliance.

2. Introduction of the “Tax Year” Concept

Old Act (1961):

The system used two different terms:

- Financial Year (FY)

- Assessment Year (AY)

This dual concept often caused confusion among taxpayers.

New Act (2025):

The new law replaces both FY and AY with a single term:

➡️ Tax Year

Impact:

- Simplifies tax filing and understanding

- Eliminates confusion

- Aligns India with global tax practices

3. Reduction in Number of Sections

Old Act:

Contained a large number of sections, many of which became redundant over time.

New Act:

- Removes obsolete provisions

- Consolidates similar sections

- Reorganizes content for better clarity

Impact:

A more streamlined law that is easier to navigate and interpret.

4. Updated Income Tax Rules (2026 Alignment)

The new Act works alongside Income Tax Rules, 2026, which modernize deduction limits and compliance requirements.

Key Updates Include:

- Higher limits for allowances (education, hostel, meals)

- Revised perquisite valuation rules

- Updated reporting formats

- Improved PAN-related compliance

Impact:

Better alignment with current economic realities and improved tax efficiency for salaried individuals.

5. Changes in Tax Compliance and Filing

Old Act:

- Complex filing procedures

- Multiple forms and overlapping requirements

- Tight deadlines

New Act:

- Simplified filing structure

- Revised ITR deadlines

- Extended timelines for certain taxpayers

Example:

- ITR-3 & ITR-4 due date extended to 31 August (non-audit cases)

Impact:

Reduced compliance burden and improved accuracy in filings.

6. Improved Transparency and Reduced Litigation

Old Act:

- Frequent disputes due to ambiguous provisions

- Heavy reliance on judicial interpretations

New Act:

- Clear drafting of provisions

- Reduced ambiguity

- Better-defined rules

Impact:

- Fewer tax disputes

- Faster resolution

- Increased trust in the tax system

7. Changes in Taxation of Investments

Old Act:

Different tax treatments existed for various financial instruments, sometimes leading to confusion.

New Act:

Introduces clarity and consistency in areas such as:

- Buyback taxation (treated as capital gains)

- Sovereign Gold Bonds (limited exemption benefits)

- Dividend taxation (removal of interest deduction)

Impact:

- Clearer tax treatment

- Better financial planning

- Reduced loopholes

8. Revised TCS and STT Framework

Old Act:

TCS and STT structures were complex and sometimes led to higher refunds and confusion.

New Act:

- Rationalized TCS rates

- Increased STT rates (especially for derivatives)

- Simplified tax collection mechanism

Impact:

- Improved compliance

- Reduced refund delays

- Increased cost for traders

9. Modernized Reporting and Documentation

Old Act:

- Traditional reporting formats

- Limited integration with digital systems

New Act:

- Introduction of updated forms

- Renaming and restructuring of key documents

- Better digital compatibility

Examples:

- Form 16 → Form 130

- Form 26AS → Form 168

Impact:

- Improved data tracking

- Better integration with digital platforms

- Enhanced transparency

10. Focus on Digital and Automated Compliance

Old Act:

- Manual processes dominated

- Limited automation

New Act:

- Increased digital integration

- Automated compliance checks

- Enhanced data matching

Impact:

- Faster processing of returns

- Reduced human error

- Better monitoring by tax authorities

11. Changes Benefiting Salaried Individuals

The new Act provides several advantages for salaried taxpayers:

- Increased allowance limits

- Simplified compliance

- Clearer salary structure taxation

Impact:

Higher take-home benefits and easier tax planning.

12. Impact on Businesses and Professionals

Businesses and professionals will experience:

- Simplified compliance requirements

- Extended filing deadlines

- Reduced legal complexities

Impact:

More time for accurate filings and reduced compliance stress.

13. Impact on Investors

Investors will see both advantages and challenges:

Positive:

- Clearer taxation rules

- Better transparency

Negative:

- Higher STT rates

- Reduced deductions on dividend income

Impact:

Investors must reassess strategies to optimize tax efficiency.

Key Differences at a Glance

Aspect | Income Tax Act 1961 | Income Tax Act 2025 |

Structure | Complex | Simplified |

Terminology | FY & AY | Tax Year |

Language | Legal-heavy | Easy to understand |

Compliance | Complicated | Streamlined |

Litigation | High | Reduced |

Digital Integration | Limited | Advanced |

Reporting | Traditional | Modernized |

What Taxpayers Should Do Now

To adapt to the new system, taxpayers should:

- Stay updated with new rules and deadlines

- Understand the Tax Year concept

- Review investment strategies

- Ensure accurate documentation

- Use digital tools for compliance

Early preparation will help avoid errors and maximize tax savings.

Conclusion

The transition from the Income Tax Act, 1961 to the Income Tax Act, 2025 marks one of the most significant reforms in India’s taxation history. The new framework focuses on simplicity, transparency, and efficiency, making the system more user-friendly for all categories of taxpayers.

While the new law reduces complexity and improves compliance, certain changes—such as revised taxation on investments and increased transaction taxes—may increase the burden for some individuals.

Overall, the reform is a positive step toward a modern and streamlined tax system. Taxpayers who understand these changes early will be better positioned to plan their finances effectively and stay compliant in the evolving tax landscape.